£1,000 Capital Gains in 2025 – My Investment Strategy

It’s taken some time but I am eventually in a position where I have nearly £20k available to invest. It is a great feeling and just in case I have not made myself clear at any point, I will repeat until I am blue in the face that this is money which came from nowhere and I did not have to work for. How did it all come to be?

- I have deposited the entirety of my Free Money Earnings in a basket of ISA accounts which I call the Free Cash Fund. This Fund has grown slowly but surely and is valued at £10.5k at the time of writing these lines (January 2025).

- Having that money available allows me to use it as collateral to build a Stoozing Fund. That is me taking advantage of 0% Balance Transfer Credit Cards Offers to contract a debt and deposit that sum in risk free hight interest savings accounts in view to making a profit using funds that I do not have. The Stoozing Fund is valued at £8k.

The Free Cash Fund came first which in turn paved the way for me to start the Stoozing Fund from scratch. To build up the Free Cash Fund from £0 to £10.5k I used a very basic Investment Strategy where 60% of earnings where deployed into a Cash ISA, 30% into Stocks & Shares ISAs and 10% was kept as cash (see post How to Invest the Free Cash Fund to target a 5% growth). My goal was a 5% growth but I am extremely pleased to report that the Fund has yielded £917 in gains or a 9.6% growth.

“The Free Cash Fund has grown by 9.6% delivering £917 Net Gains”

Well, if the Investment Strategy is working nicely, why change it? It is a little bit of both: I am keeping things as they are but I also need to deploy my Free Money Earnings in a slightly different way. Let me explain the reasons behind this adjustment.

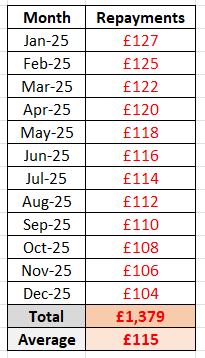

Stoozing Fund debt Repayment Plan

I took on £7,500 of debt from credit cards in 2024, £2,500 in March and an additional £5,000 in December. For a detailed explanation of my Stoozing methods, see posts:

- How to make Free Money from Credit Cards – Stoozing 3.0

- How to make Free Money from Credit Cards – Stoozing 2.0

This money is deposited in a number of risk-free high-interest savings accounts. I will be profiting from interest payments and that essentially is the whole point of Stoozing.

I have used stoozing methods to make free money systematically in the past. Stoozing was always on the back of my mind since the very first moment I started documenting my Journey in this Blog. There are two basic reasons why I was not able to start stoozing earlier:

- Savings accounts interest rates only started to pick up in 2023/2024.

- The Cash Reserves Pot (remember: 10% of my Free Money Earnings deployed here) was not big enough to service any kind of credit card repayment.

Let’s elaborate a little bit more on point number 2. The fact that I am transferring a balance from a credit card attracts a minimum monthly repayment on the card balance. This is usually 1% or 2%. So for example, if I transfer £10,000 from the credit card and I need to pay 1% back on a monthly basis, I will pay £100 the first month, £99 the second, £98 the third, and so on. Over the course of a year I would need £1,100 of my ‘own’ money for credit card repayments. If the balance transfer promotional period is 24 months I will then need to come up with £2,000 to use a round number.

So what is my actual debt repayment situation at the moment?

- £2,500 from RBS, 1% repayment: approx £25/month

- £5,000 from Virgin, 2% repayment: approx £100/month

Monthly repayments decrease as the remaining balance is reduced. In real numbers, my credit card repayment plan over the next 12 months is shown on the table below:

It is not going to be a 2025 fad. The Stoozing Fund is here to stay and get bigger in size. So if I am planning to make £1,500 Free Money per year, the 60/30/10 rule will not do anymore by allocating just £150 (10%) to the Cash Reserves Pot. I obviously need to divert more of my earnings as cash reserves so that repayments are made and the Stoozing Fund can grow further. The question is: how much do I need?

Ok, my short term goal is to grow the Stoozing Fund to £15k. Let’s assume that I need to pay 1% back on a monthly basis over 24 months. The Cash4Nothing Stoozing Calculator throws the followings numbers:

- Net Profit: £1,058

- Total Investment: £3,326

- ROI: 32%

- Break Even: 8 months

My funding needs are going to be £2,300 (£3.3 required – £1k I currently hold) over the next 24 months. In other words, £1,000 of my £1,500 annual Free Money Earnings need to be diverted to the Cash Reserves Pot.

I have my answer now: 70% of my Free Money Earnings will need to be allocated to the Cash Reserves Pot.

That is the only adjustment required. The remaining 30% of earnings will be deposited in S&S ISAs.

What about the Free Cash Fund? Stays as is and will grow from capital gains and contributions to the S&S ISA Pot.

£1,000 Capital Gains in 2025

These gains are feasible and more importantly, they will come as Passive Income.

- £10.5k deposited in the Free Cash Fund at 5% per year: £500

- £8k in the Stoozing Fund. Profits Projection: £350

I am asking for £1,000 meaning that I am £150 short. It is a fact that both Funds will grow in 2025:

- The Free Cash Fund by £400 from Free Money Earnings contributions.

- The Stoozing Fund from taking on additional debt. Plan is to deposit £2,500 to £5,000.

It is also important to note that leverage is the main factor at play:

I am only using £11k of my ‘own money’ to generate a 10% yield.

Will my plan work? We will find out in a year’s time. For the time being, let’s write these numbers down: £917 Free Cash Fund Gains and -£162 Stoozing Fund Net Profit.

Let’s see what happens in 12 months from now.